Buy now, pay later – Is it here to stay?

DISCLAIMER: Articles are written to reflect the interests and views of the author(s), and are not intended as an official Payments Canada statement or position.

Summary 1

Buy now, pay later (BNPL) is a popular payment option offered by retail merchants to their customers for both online and in-store purchases in many regions around the world. More and more consumers globally are opting to use BNPL services, and it is expected to account for three per cent of global e-commerce spend by 2023.2 In Canada, BNPL services are gradually beginning to emerge with the potential for rapid adoption and growth. Currently, close to one in five Canadians (17 per cent) are aware of, but have not used BNPL services, while another 14 per cent of Canadians have used a BNPL service for their purchases. Among those who do not use BNPL services, three in ten indicate they would likely start using a BNPL service.3 It is estimated that “BNPL will grow 55 per cent annually in Canada, with its value increasing from US$2.5 billion in 2020 to upwards of US$17.6 billion by 2028.”4 Still, many questions remain about the value and benefits of BNPL services when weighed against the risks to both Canadian consumers and merchants. In this paper, we provide an overview of BNPL and how it works, compare BNPL with other payment installment options, examine the benefits and risks to consumers and merchants of using BNPL services, as well as examine BNPL trends outside of Canada.

BNPL is a form of short-term loan in which consumers pay for their purchases at a later date through a series of payment installments. These payments are structured in such a way that the payment amounts are equal, and the payment due dates follow a pre-set schedule, with the first payment due at checkout.5 The BNPL model involves two key players: the merchant, and the BNPL provider (usually a fintech or financial institution). The BNPL service is offered during a purchase through the merchant who partners with the BNPL provider. Figure 1 illustrates the process flow of the BNPL payment experience for online purchases.

At checkout, the customer chooses to pay in installments using a buy now, pay later method. The customer is redirected to the buy now, pay later method’s site or app to create an account or log in. They can accept or decline the terms of the repayment plan and return to the checkout flow at the merchant site.6

Typically, the customer is required to complete a short online application form either at the merchant or BNPL provider’s site. The customer provides basic personal information and a payment method, such as a debit or credit card, from which installments will be withdrawn. A soft credit check, which doesn’t affect the customer’s credit rating, might also take place. An approval decision is made on the spot. If the customer is approved, he/she can begin using the BNPL service on multiple purchases and on multiple retail sites that are partnered with that same BNPL provider.7

Figure 1: BNPL Payment Experience8

Merchants generate greater overall sales revenue in principle by offering BNPL to their customers. This outcome is achieved in three ways:

- Consumers are more likely to make a purchase;

- Consumers are likely to spend more money per shopping visit; and

- Consumers are likely shopping more regularly.9

BNPL providers collect their revenue mainly from the fees they charge the merchants that accept the loans as a customer payment option. Additional revenue is obtained from late fees or penalties charged to consumers who do not fulfill the repayment terms.10

In Canada, the BNPL market is dominated by a handful of BNPL providers: PayBright, Afterpay, Sezzle, and Affirm. However, other financial institutions like banks are entering the market, for example, CIBC, which launched the Pace It feature on its credit cards in 2019; Scotiabank with its SelectPay program, which works similarly to Pace It; and PayPlan by RBC, which offers consumers a pay-over-time option for big-ticket purchases at online retailers throughout Canada.11

Global payment companies have also entered the market. Mastercard launched a BNPL program “allowing users to pay for purchases in interest-free installments on their debit, credit and prepaid cards.”12 Visa launched a similar program called Visa Installments, while PayPal offers its Pay in 4 BNPL service.13

BNPL services are similar in many ways to existing installment payments, such as layaway and credit cards. A layaway program is a “pay-over-time service offered by a merchant that allows a consumer to reserve an item by making interest-free, predetermined installment payments until the item is paid for in full.”14 The consumer takes possession of the item after all of the installment payments are made. Layaway enables consumers to obtain an item that they might not otherwise be able to afford, while avoiding going into debt. As such, layaway represents a low risk for both the consumer and merchant. The only potential costs charged to the consumer are: a non-refundable service fee; and a cancellation fee if the consumer does not complete the purchase. In the case of the merchant, “layaway enables sales that might not occur otherwise; however, if the consumer fails to pay in full, the value of the good may decrease over the loan term.”15 Although still available, layaway programs swiftly began to decline during the 1980s when credit card usage became more mainstream.16

BNPL services also share similarities with credit cards, in that credit cards enable consumers to immediately take possession of goods and delay payment. Credit card users can carry a balance from month to month, choosing to repay it in installments. For many Canadians, credit cards are a popular option for installment payments because they may also offer cash back or travel rewards. But, to obtain a credit card, consumers must qualify to be credit worthy by meeting a minimum credit score threshold. Layaway and BNPL services provide a way for a larger segment of the population – especially those with poor or no credit – to access goods and services. In general, “interest-free BNPL services and layaway are comparable in their terms and costs, but BNPL enables consumers to take immediate possession of a product at the point-of-purchase while layaway requires consumers to wait until the product has been paid for in full.”17 If using layaway requires a service fee, then BNPL can be the least expensive method of payment.18

Benefits and risks to consumers

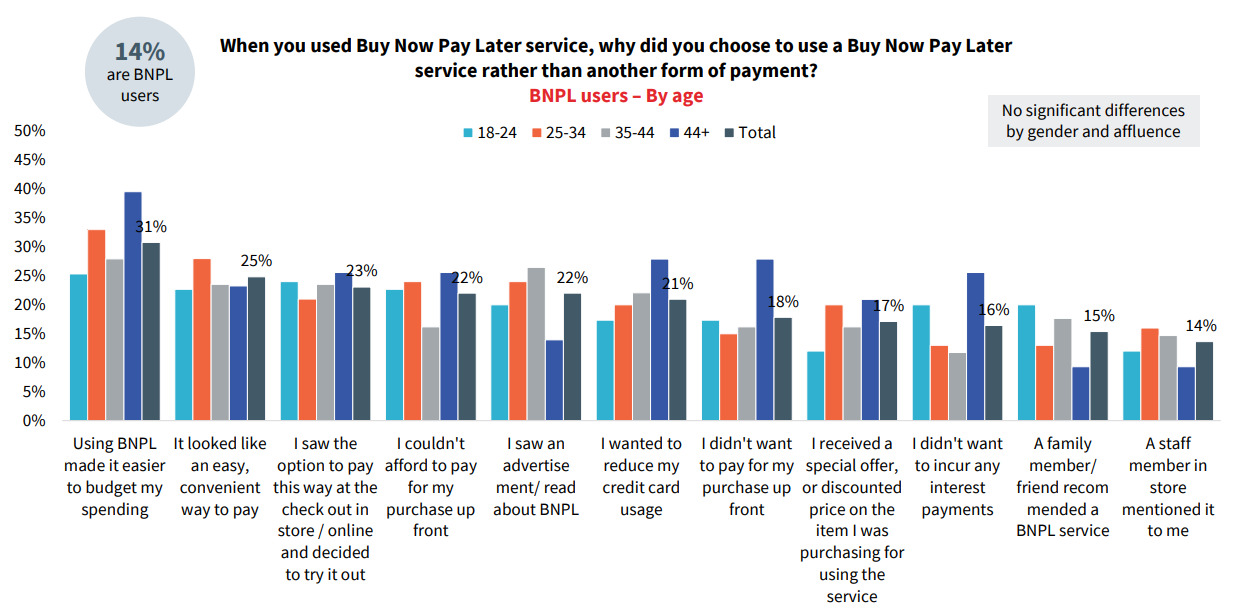

In Canada, BNPL users fit a discernible profile. They tend to be younger (18-34), are non-credit cardholders, and belong to either the mass market or mass affluent groups.19 BNPL services provide various benefits to consumers including:

- Makes it easier to budget spending because the payment streams are predictable (follows a set amount and time frame), and some BNPL apps come with budgeting tools.

- Is a convenient way to pay – the BNPL payment option is embedded in the e-commerce platform and consumer application and approval usually takes a few minutes to complete (compared to days for credit card approvals).

- Makes it possible for consumers to afford to pay for purchases upfront. For Canadians who either do not have access to traditional forms of credit (e.g., credit card, personal line of credit), or have lower incomes, BNPL allows them to make purchases that otherwise would not fit their budget.20

These key benefits are what drives Canadians towards using BNPL services as opposed to another form of payment (see Figure 2). Consumers cite interest avoidance, payment deferral, and reducing credit card usage as other reasons for using BNPL services.21 Another key benefit of BNPL services involves consumers who do not have access to credit. Unlike layaway, BNPL enables consumers to immediately take possession of a product as they are still paying for it. This is an important benefit for consumers making larger value purchases and who do not have a credit card.

Figure 2: Drivers of BNPL Usage22

For users with little or no credit or poor credit history, some BNPL providers in the U.S. have started to offer programs for its customers to send their repayment history to a credit agency to help build their credit file and improve their credit score.23 If Canadian BNPL providers followed this same practice, it would mean greater access to credit for Canadians overall.

With the many consumer benefits of using BNPL services, there are also risks. BNPL providers are not obligated to qualify a consumer’s ability to repay loans, unlike credit card providers. The majority of BNPL providers do not look up an applicant’s credit report during the adjudication process. Rather, a soft credit check is performed.24 So, if the eligibility requirements for obtaining a BNPL short-term loan is not as rigorous as traditional credit card or loan applications, consumers with bad or no credit might easily be approved. As a result, these consumers potentially can find themselves getting into an unmanageable debt load if they use multiple BNPL services. According to a recent U.S. consumer research study conducted among BNPL users by Piplsay, 74 per cent of those surveyed made all of their BNPL payments on time, 14 per cent missed a payment once, and 12 per cent missed a payment more than once.25

In general, Canadians’ borrowing intentions are increasing, with almost three in five consumers (58 per cent) indicating they plan to borrow more money before the end of this year, according to the latest MNP Consumer Debt Index report.26 Moreover, BNPL purchases spiked during the COVID-19 crisis with an uptick in online shopping, a trend that is likely to continue into the 2021 holiday shopping season.27

Another potential risk for consumers is that “the availability of BNPL credit during the checkout process could encourage impulse buying.”28 In another recent U.S. study of BNPL users, 16 per cent of them made five or more purchases with BNPL in an average month.29 BNPL users who make multiple purchases using different BNPL providers might find it difficult to keep track of and manage all of their purchases, which might lead to late and missed payment fees.

There are also longer-term risks associated with BNPL services. BNPL users are typically younger, so their ability to obtain credit or even certain types of employment in the future might be put at risk if they run into financial trouble.30 Some BNPL providers such as Sezzle do not report its customers’ payment activities to credit bureaus. However, PayBright, Afterpay and Affirm do report customers that either default on their loan or make a late payment to credit bureaus, which affects their credit scores and reduces their chances of getting a future loan.31

Benefits and risks to merchants

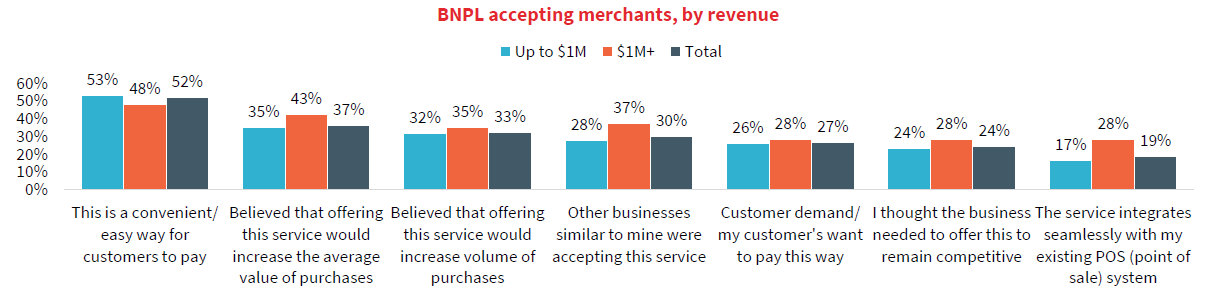

BNPL services provide a number of demonstrable benefits to merchants. According to a study by BNPL providers, merchants experience a lower cart abandonment rate and higher repeat business when offering BNPL as a payment option to their customers.32 The predictable nature of BNPL repayments (i.e., fixed dollar installments to be repaid over a predefined time frame) potentially make consumer goods more obtainable, and help increase consumer purchase propensity and transaction value.33 Another benefit of BNPL services is that merchants are able to settle sales quickly, and it may “eliminate a merchant’s chargeback and fraud risks because BNPL providers assume those risks.”34 As BNPL services increase in popularity, particularly among younger consumers, merchants may gain or maintain a competitive advantage by offering BNPL as a payment option, because consumers may choose to only shop at merchants that offer BNPL. Merchants can also benefit from having BNPL providers directly market their product offers to consumers. Furthermore, BNPL services “with direct API integration capabilities (which allow different apps to exchange data) enable merchants to offer consumers a seamless checkout experience: the consumer can apply for a loan, receive the loan approval, and pay for the first installment easily and quickly during checkout.”35 This has resulted in a growing number of merchants, including big-box retailers such as Amazon and Walmart, to begin offering BNPL as a payment option for both on-line and in-store purchases.36 In a recent merchant survey by RFi, close to one in ten merchants (eight per cent) indicated that they accept BNPL as a payment option, while 48 per cent of those that do not offer customers the option to pay by BNPL said they are either interested or extremely interested in offering BNPL to their customers.37 Figure 3 illustrates the key drivers of BNPL acceptance among Canadian merchants.

Figure 3: Drivers of BNPL Acceptance38

Despite the potential benefits to merchants of accepting BNPL from their customers, there are associated risks as well. The cost of a BNPL transaction for merchants can be anywhere from two per cent to eight per cent of the purchase price of the item sold. By comparison, the typical cost of a credit or debit card transaction is between one and three per cent.39 Therefore, merchants rely on a bump in their overall sales volume, so that the increased revenue helps to more than offset the increased transaction cost. Related to this point is the risk that having a BNPL payment option will cause existing customers to switch away from payment options, such as credit, debit and prepaid cards, that cost the merchant less to accept.

Before embarking on a BNPL strategy, merchants need to consider whether BNPL services is a good fit with what they’re selling, and determine the minimum transaction value required to justify offering BNPL as a payment option.40 The aim of merchants in offering BNPL as a payment option is to acquire new customers. While this might be achievable, BNPL providers “may cap the number of concurrent loans a consumer can have, which can limit a merchant’s ability to maintain a recurring relationship.”41

Another risk for merchants to consider is that over time they may reach a point at which the cost of accepting BNPL outweighs the value. But once BNPL becomes entrenched as a widely used payment method by consumers, “merchants may not be able to discontinue accepting it even if the cost has become greater than the benefit, and the cost may not decline without regulatory intervention.”42 Lastly, there is the risk of harming the customer relationship in the case of product returns when BNPL services are involved. BNPL purchases have shown to yield a lower return rate but, when returns do occur, the process can be especially cumbersome for the customer due to the extra steps involved. In some cases, BNPL providers might still hold the customer liable for the total cost of a purchase even after the item has been returned.43

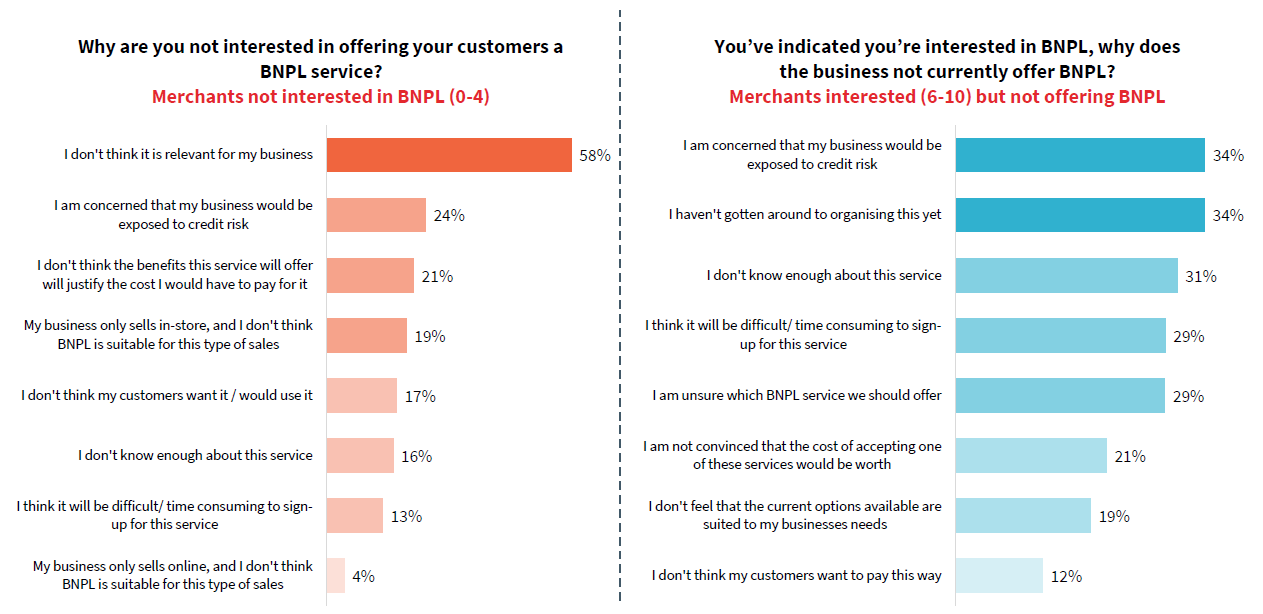

Merchants that are interested in BNPL but do not currently offer it to their customers appear to have a misconception about a key risk associated with BNPL. When asked why they are not currently offering their customers a BNPL service, about one in three merchants (34 per cent) indicated that they were concerned that their business would be exposed to a credit risk (see Figure 4).44 Since it is the BNPL provider and not the merchant that assumes the risk of a customer defaulting on their loan payments, this result implies that more education is required to provide merchants with a clearer understanding of the BNPL model. Among merchants that are not interested in BNPL, the primary reason for choosing not to offer their customers this payment option is because they do not think it is relevant for their business.45

Figure 4: Barriers to Merchant Acceptance of BNPL46

BNPL international trends

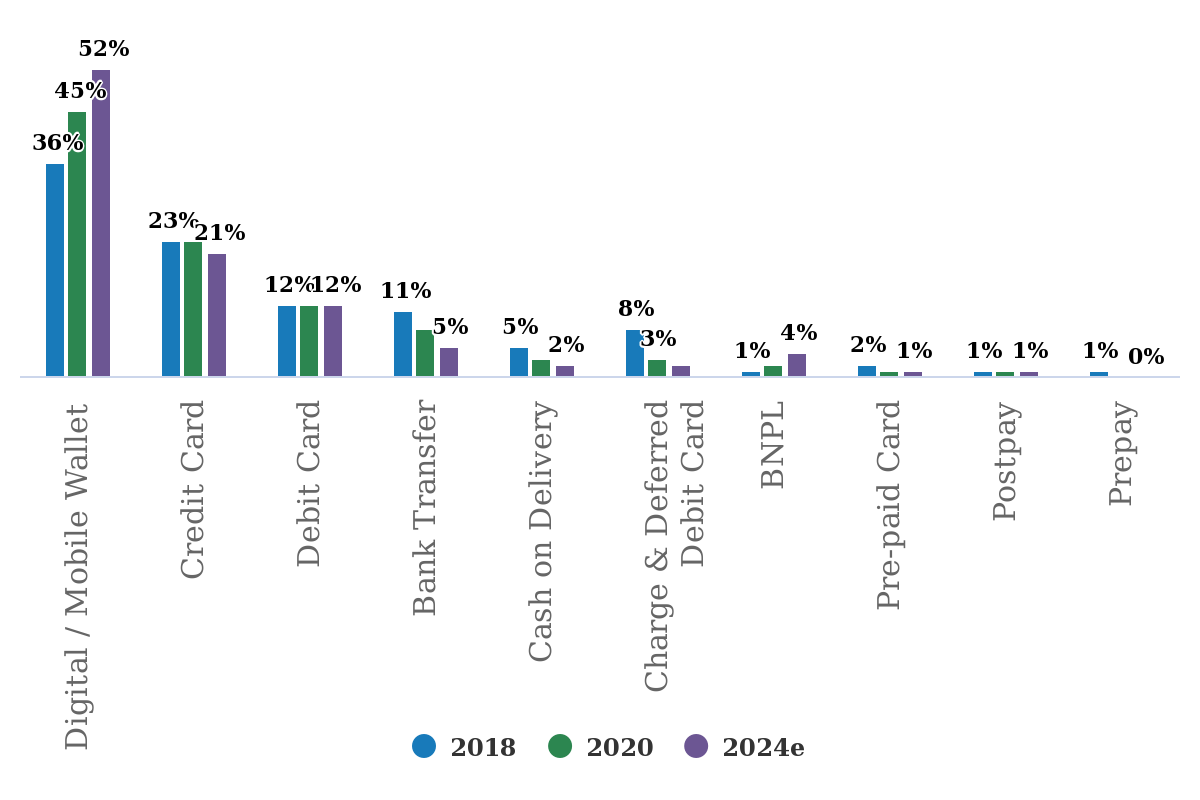

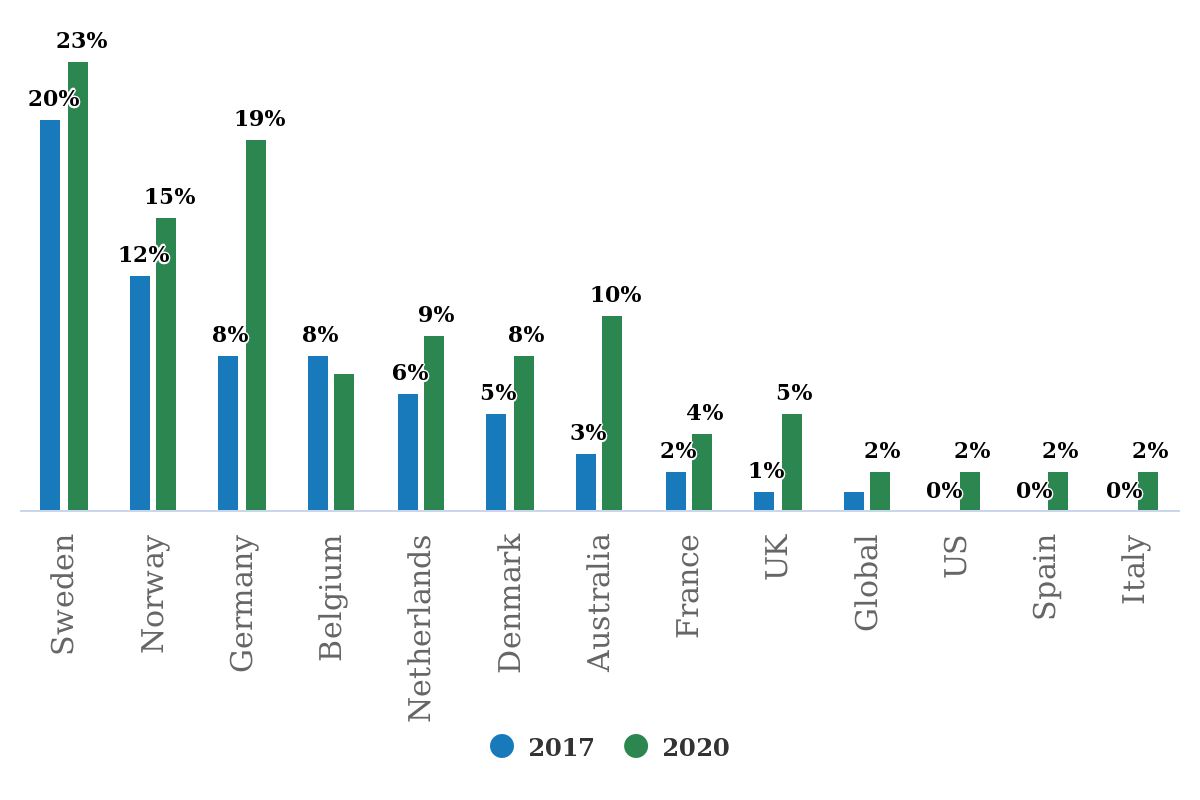

Although BNPL services are relatively new in Canada, installments have been in use for some time in Europe and South America. For instance, half of all credit card purchases made in Brazil are on installment payments.47 Overall, installments represent an important segment of the global payments market. In 2019, it comprised $1.7 trillion CAD in global payments volume, and global adoption is growing two and a half times faster than traditional card payments.48 Currently, BNPL accounts for two per cent of total global online purchases, but it is the fastest growing payment method globally, and some European markets are seeing the highest adoption: 23 per cent in Sweden, and 19 per cent in Germany (see Figures 5 and 6).49

Figure 5: Global Payment Method Usage For Online Purchases50

Figure 6: BNPL Usage For Online Purchases By Country51

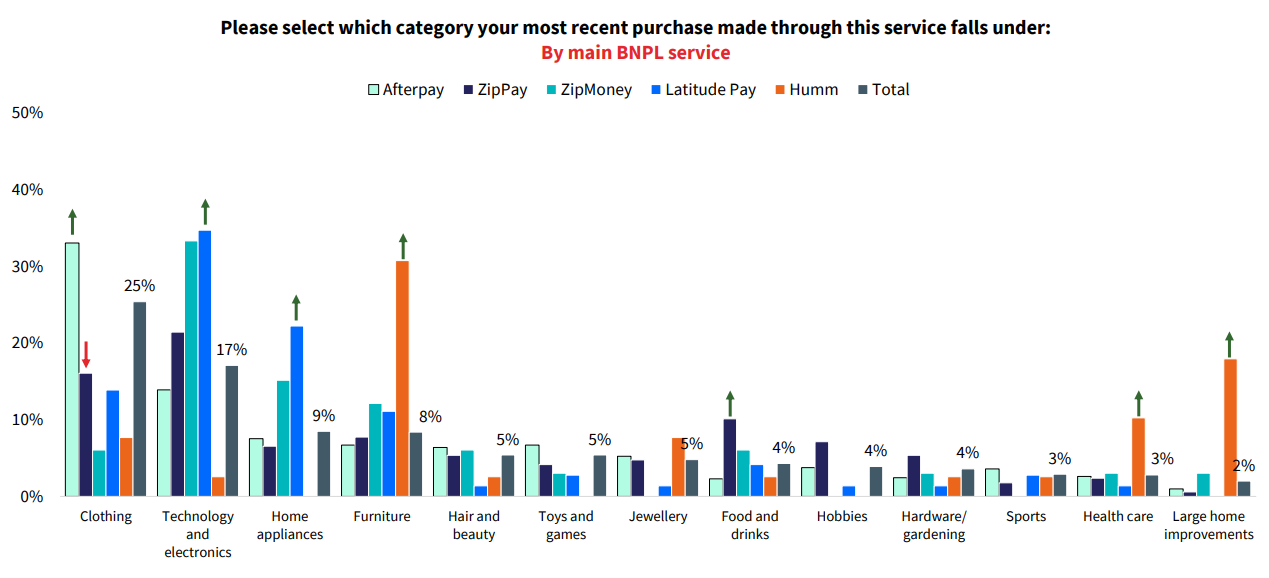

Both the Australian and U.S. markets provide good examples of how BNPL services have matured over time and offer a glimpse into how the Canadian BNPL market might develop in the near future. In Australia, awareness of BNPL services has reached almost universal levels, with 92 per cent of the population indicating that they are aware of BNPL.52 Medium to long term growth of the BNPL market is expected to remain strong, with BNPL consumer adoption projected to increase at a compound annual growth rate of 24 per cent from 2021-2028.53 This forecasted growth is fueled in part by a “favourable regulatory framework and the presence of the world’s leading BNPL companies.”54 For historical context, the total BNPL payment transaction volume in Australia nearly doubled from 16.8 million in the 2017-18 financial year to 32 million in 2018-19, reflecting an increase of 90 per cent.55 The most common purchase categories involving BNPL services are clothes and technology/electronics (see Figure 7).

Figure 7: Types of Purchases BNPL Used For - Australia56

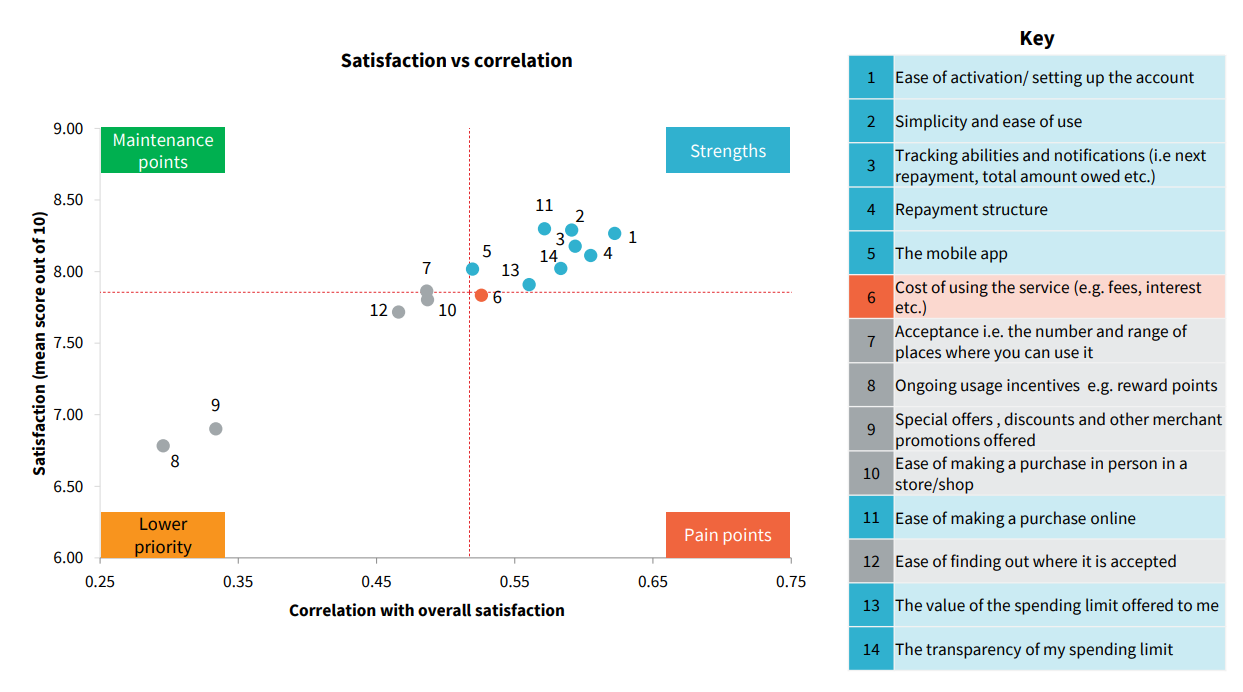

In general, BNPL providers perform well in those areas of the BNPL user experience that drives satisfaction (see Figure 8). These include making it easy to set up and activate an account; simplicity of use; tracking abilities and notifications (e.g., when next repayment is due, total amount owing); and the repayment structure.57

Figure 8: Key Drivers of BNPL User Satisfaction - Australia58

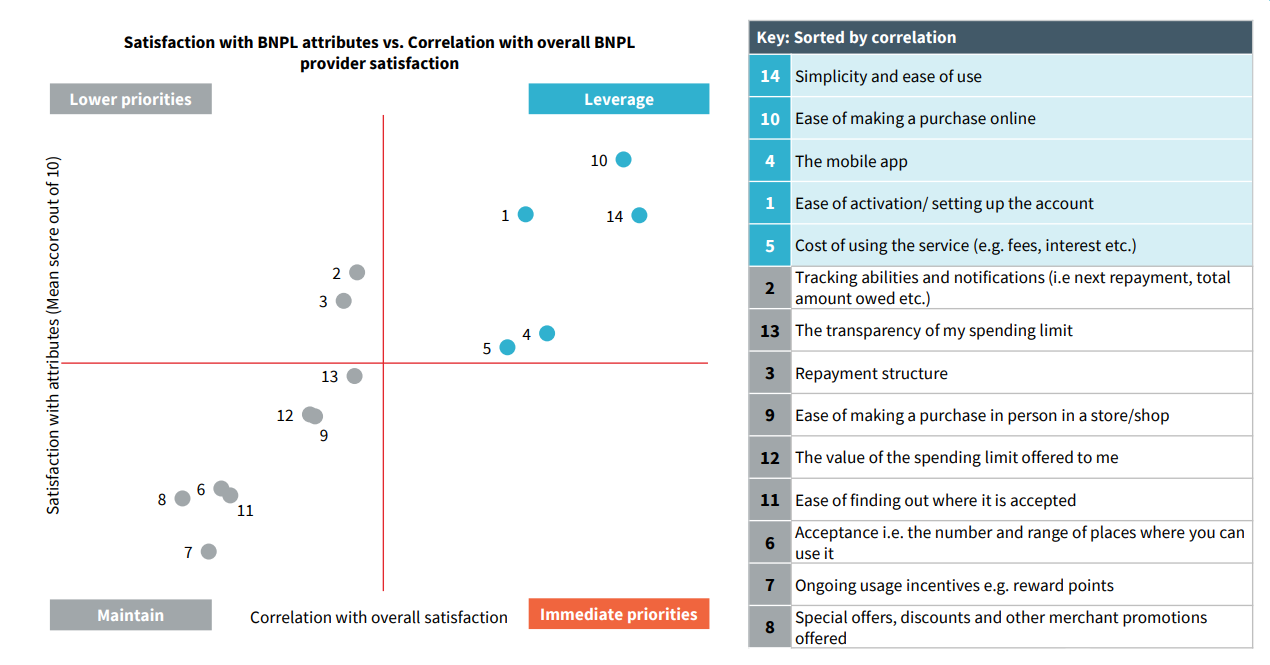

In the U.S., awareness of BNPL services is not nearly as high as that of Australia, with 56 per cent of the population indicating that they are aware of BNPL.59 Many consumers have used BNPL services and the number of adopters continues to quickly expand. Since 2018, the number of BNPL users in the U.S. has been growing by over 300 per cent each year, reaching 45 million active users in 2021.60 The total BNPL payment transaction value has also increased and now accounts for close to two per cent of total U.S. online merchant sales.61 BNPL users in the U.S. tend to be “predominantly female and younger, with the vast majority being millennials and Gen Z consumers.”62 They are also more likely to be consumers with lower incomes, and who lack access to traditional forms of credit (e.g., credit card, personal line of credit) or banking services.63 In general, BNPL providers perform well in those areas of the BNPL user experience that drive satisfaction (see Figure 9). However, these key drivers slightly differ from those in Australia. These include making it easy to set up and activate an account; simplicity of use; and ease of making a purchase online. Low cost of using BNPL services and the mobile app user experience are also important here, but tracking abilities and notifications is less so.64

Figure 9: Key Drivers of BNPL User Satisfaction – U.S.65

Conclusion

BNPL use is expected to continue to grow as an alternative payment method because of its compelling customer value proposition – easier to qualify for BNPL loans than traditional forms of credit; ease of set-up and activation; ability to pay using BNPL at many popular merchant partners; and easier to budget spending.

There are benefits to both consumers and merchants for adopting BNPL, but BNPL is still new enough in Canada that the risks are not widely understood. Understanding the ins and outs of using BNPL is important in order for consumers and merchants to effectively manage these risks.

In other more established BNPL markets around the world (e.g., Australia, United Kingdom, U.S.), there have been calls for more regulatory intervention by the government, as well as action on the part of BNPL providers to address the rising tide of younger BNPL users accumulating more debt, and being worse off financially. For instance, in the U.S., the Consumer Financial Protection Bureau has encouraged BNPL providers to take steps to ensure users are adequately informed of the risks BNPL presents.66 While in Australia, a group of eight of the largest BNPL companies signed up to a voluntary code of practice. “The code sets out the minimum standards the companies need to meet, including a cap on late fees, credit checks being required on transactions of more than $2,000 and a minimum age of 18 years for customers to be able to use the services.”67

The lessons learned in these markets provide useful insights and can help create a roadmap for how BNPL providers, merchants, and policy-makers in Canada approach implementing BNPL services for the benefit of all. A call for more regulatory intervention to protect Canadians against the risks associated with BNPL use needs to be balanced against the potential impact it will have on stifling payments innovation and market competition. However, a basic truth that BNPL providers, merchants, and policy-makers can all agree on is that consumers should not be using their discretionary spending on the things they cannot afford. And while it is not feasible to tell consumers what they should or shouldn’t buy, BNPL providers, merchants, and policy-makers have the power to create a sensible and fair approach for approving BNPL loans to Canadians based upon their ability to repay with minimal hardship.

1 The views presented in this paper are those of the authors and do not necessarily reflect the views of Payments Canada.

2 FIS, Worldpay from FIS 2020 Global Payments Report, April 22, 2021. https://www.auspaynet.com.au/insights/blog/BNPL2021.

3 RFi, BNPL Consumer Report 2021, September 2021.

4 Research and Markets, Canada Buy Now, Pay Later Market Report 2021, November 12, 2021. https://www.moneysense.ca/spend/buy-now-pay-later/.

5 J. Alcazar and T. Bradford, The Appeal and Proliferation of Buy Now, Pay Later: Consumer and Merchant Perspectives, Federal Reserve Bank of Kansas City, November 10, 2021. https://www.kansascityfed.org/research/payments-system-research-briefings/the-appeal-and-proliferation-of-buy-now-pay-later-consumer-and-merchant-perspectives/.

6 Stripe, Buy Now, Pay Later Payment Experience, 2021. https://stripe.com/docs/payments/buy-now-pay-later.

7 S. Nicholls Jones, Be Cautious When Using Buy-Now-Pay-Later For Online Purchases, Chartered Professional Accountants Canada, October 29, 2021. https://www.cpacanada.ca/en/news/canada/2021-10-29-buy-now-pay-later-trend.

8 Stripe, Buy Now, Pay Later Payment Experience, 2021. https://stripe.com/docs/payments/buy-now-pay-later.

9 A. Mull, Why Is There Financing For Everything Now?, The Atlantic, December 15, 2020. https://www.theatlantic.com/magazine/archive/2021/01/jeans-now-pay-later/617257/.

10 J. Alcazar and T. Bradford, The Appeal and Proliferation of Buy Now, Pay Later: Consumer and Merchant Perspectives, Federal Reserve Bank of Kansas City, November 10, 2021. https://www.kansascityfed.org/research/payments-system-research-briefings/the-appeal-and-proliferation-of-buy-now-pay-later-consumer-and-merchant-perspectives/.

11 C. Reilly-Larke, Buy Now, Pay Later: Are Installment Plans a Budget Win or Finance Fail? November 12, 2021. https://www.moneysense.ca/spend/buy-now-pay-later/.

12 Ibid.

13 Ibid.

14 J. Alcazar and T. Bradford, The Appeal and Proliferation of Buy Now, Pay Later: Consumer and Merchant Perspectives, Federal Reserve Bank of Kansas City, November 10, 2021. https://www.kansascityfed.org/research/payments-system-research-briefings/the-appeal-and-proliferation-of-buy-now-pay-later-consumer-and-merchant-perspectives/.

15 Ibid.

16 C. Reilly-Larke, Buy Now, Pay Later: Are Installment Plans a Budget Win or Finance Fail? November 12, 2021. https://www.moneysense.ca/spend/buy-now-pay-later/.

17 J. Alcazar and T. Bradford, The Appeal and Proliferation of Buy Now, Pay Later: Consumer and Merchant Perspectives, Federal Reserve Bank of Kansas City, November 10, 2021. https://www.kansascityfed.org/research/payments-system-research-briefings/the-appeal-and-proliferation-of-buy-now-pay-later-consumer-and-merchant-perspectives/.

18 Ibid.

19 RFi, BNPL Consumer Report 2021, September 2021.

20 Ibid.

21 Ibid.

22 Ibid.

23 J. Alcazar and T. Bradford, The Appeal and Proliferation of Buy Now, Pay Later: Consumer and Merchant Perspectives, Federal Reserve Bank of Kansas City, November 10, 2021. https://www.kansascityfed.org/research/payments-system-research-briefings/the-appeal-and-proliferation-of-buy-now-pay-later-consumer-and-merchant-perspectives/.

24 S. Nicholls Jones, Be Cautious When Using Buy-Now-Pay-Later For Online Purchases”, Chartered Professional Accountants Canada, October 29, 2021. https://www.cpacanada.ca/en/news/canada/2021-10-29-buy-now-pay-later-trend.

25 J. Alcazar and T. Bradford, The Appeal and Proliferation of Buy Now, Pay Later: Consumer and Merchant Perspectives, Federal Reserve Bank of Kansas City, November 10, 2021. https://www.kansascityfed.org/research/payments-system-research-briefings/the-appeal-and-proliferation-of-buy-now-pay-later-consumer-and-merchant-perspectives/.

26 MNP, MNP Consumer Debt Index (Wave 18), October 2021. https://mnpdebt.ca/en/resources/mnp-consumer-debt-index.

27 G. Bazian, Low Interest Rates And Rising Costs Leading Many Canadians Down Ever-riskier Path to Borrow More”, MNP Ltd., October 4, 2021. https://mnpdebt.ca/en/resources/mnp-debt-blog/low-interest-rates-and-rising-costs-leading-many-canadians-down-ever-riskier-path-to-borrow-more.

28 J. Alcazar and T. Bradford, The Appeal and Proliferation of Buy Now, Pay Later: Consumer and Merchant Perspectives, Federal Reserve Bank of Kansas City, November 10, 2021. https://www.kansascityfed.org/research/payments-system-research-briefings/the-appeal-and-proliferation-of-buy-now-pay-later-consumer-and-merchant-perspectives/.

29 Ibid.

30 Ibid.

31 A. Boyd, Finty, Apr. 15, 2021. https://finty.com/ca/buy-now-pay-later/affirm-review/.

32 J. Alcazar and T. Bradford, The Appeal and Proliferation of Buy Now, Pay Later: Consumer and Merchant Perspectives, Federal Reserve Bank of Kansas City, November 10, 2021. https://www.kansascityfed.org/research/payments-system-research-briefings/the-appeal-and-proliferation-of-buy-now-pay-later-consumer-and-merchant-perspectives/.

33 Ibid.

34 Ibid.

35 Ibid.

36 Ibid.

37 RFi, “BNPL in Canada - Merchant Report 2021” October 2021.

38 Ibid.

39 T. Kiladze, “Buy Now, Pay Later Lenders Have Some Swagger, But Their Revolution is Far From Certain in Canada”, The Globe and Mail, August 9, 2021. https://www.theglobeandmail.com/business/article-fintechs-buy-now-pay-later-revolution-is-far-from-certain/.

40 J. Alcazar and T. Bradford, The Appeal and Proliferation of Buy Now, Pay Later: Consumer and Merchant Perspectives, Federal Reserve Bank of Kansas City, November 10, 2021. https://www.kansascityfed.org/research/payments-system-research-briefings/the-appeal-and-proliferation-of-buy-now-pay-later-consumer-and-merchant-perspectives/.

41 Ibid.

42 Ibid.

43 Ibid.

44 RFi, BNPL in Canada - Merchant Report 2021, October 2021.

45 Ibid.

46 RFi, BNPL in Canada - Merchant Report 2021, October 2021.

47 B. Weiner, Thought Leadership: The Bright Future of Installments in Canada, Visa Canada. https://www.visa.ca/en_CA/about-visa/newsroom/press-releases/the-bright-future-of-installments-in-canada.html?li_fat_id=57eac14b-45c8-4a25-be82-6c7ab94f87c2.

48 Ibid.

49 Morgan Stanley, Buy Now, Pay Later: Banking on Global Financial Innovation, November 11, 2021. https://www.morganstanley.com/ideas/buy-now-pay-later-apps-credit-card-alternative.

50 Ibid.

51 Morgan Stanley, Buy Now Pay Later: Banking on Global Financial Innovation, November 11, 2021. https://www.morganstanley.com/ideas/buy-now-pay-later-apps-credit-card-alternative.

52 RFi, BNPL Consumer Report 2021, September 2021.

53 Research and Markets, Australia Buy Now, Pay Later Market Report 2021: BNPL Payment Adoption to Grow by 24 % to 2028, September 23, 2021. https://www.globenewswire.com/en/news-release/2021/09/23/2302072/28124/en/Australia-Buy-Now-Pay-Later-Market-Report-2021-BNPL-Payment-Adoption-to-Grow-by-24-to-2028.html.

54 Ibid.

55 Canstar, Buy Now, Pay Later Services, 2021. https://www.canstar.com.au/buy-now-pay-later/.

56 RFi, BNPL Consumer Report 2021, September 2021.

57 RFi, BNPL Consumer Report 2021, September 2021.

58 Ibid.

59 Ibid.

60 J. Alcazar and T. Bradford, The Appeal and Proliferation of Buy Now, Pay Later: Consumer and Merchant Perspectives, Federal Reserve Bank of Kansas City, November 10, 2021. https://www.kansascityfed.org/research/payments-system-research-briefings/the-appeal-and-proliferation-of-buy-now-pay-later-consumer-and-merchant-perspectives/.

61 Ibid.

62 Ibid.

63 Ibid.

64 RFi, BNPL Consumer Report 2021, September 2021

65 Ibid.

66 J. Alcazar and T. Bradford, The Appeal and Proliferation of Buy Now, Pay Later: Consumer and Merchant Perspectives, Federal Reserve Bank of Kansas City, November 10, 2021. https://www.kansascityfed.org/research/payments-system-research-briefings/the-appeal-and-proliferation-of-buy-now-pay-later-consumer-and-merchant-perspectives/.

67 Canstar, Buy Now, Pay Later Services, 2021. https://www.canstar.com.au/buy-now-pay-later/.

Author

Stephen Yun

Stephen Yun is a Senior Analyst, Market Insights at Payments Canada, whose areas of focus include the Consumer Payment Methods and Trends and Payment Behaviour Tracking studies, and leveraging research insights to create a consumer/business payments narrative and drive business action for his business partners. Stephen has more than 15 years of experience leading marketing and customer experience research. He has held progressively senior roles within marketing research on both the client and supplier side, serving different vertical markets (including financial services, consumer packaged goods, and educational services). He holds MBA and BBA degrees from the Schulich School of Business (York University) specializing in Marketing and Finance.